SkinBioTherapeutics PLC

SkinBioTherapeutics PLC

I told you so: The Tumultuous Saga of SkinBioTherapeutics and the Quest for Clarity Amidst Corporate Storms

By Elric Langton | 1 March 2024

Mike, Alex and I have a financial interest in SkinBioTherapeutics.

As I sat down to digest the latest episode from Tom Winnifrith’s bearcast, a sense of bewilderment washed over me, tinged with sheer frustration. The narrative spun by Tom, affectionately known as Mr Angry, paints a rather grim picture for the CEO of SkinBioTherapeutics, suggesting that his tenure might be hanging by a thread amidst a growing storm of discontent from incumbent institutions, as implied. My recent exchanges with Ashman, especially after the convertible bond announcement, contradict the current sentiments of the institutional backers, according to Tom.

Before we dive into the crux of this crucial update, I'll be sharing a screenshot at the conclusion of this piece, showcasing the censorship antics of Bristol's undercover leftist. Despite his vocal support for free speech and opposition to cancel culture, his actions tell a different story.

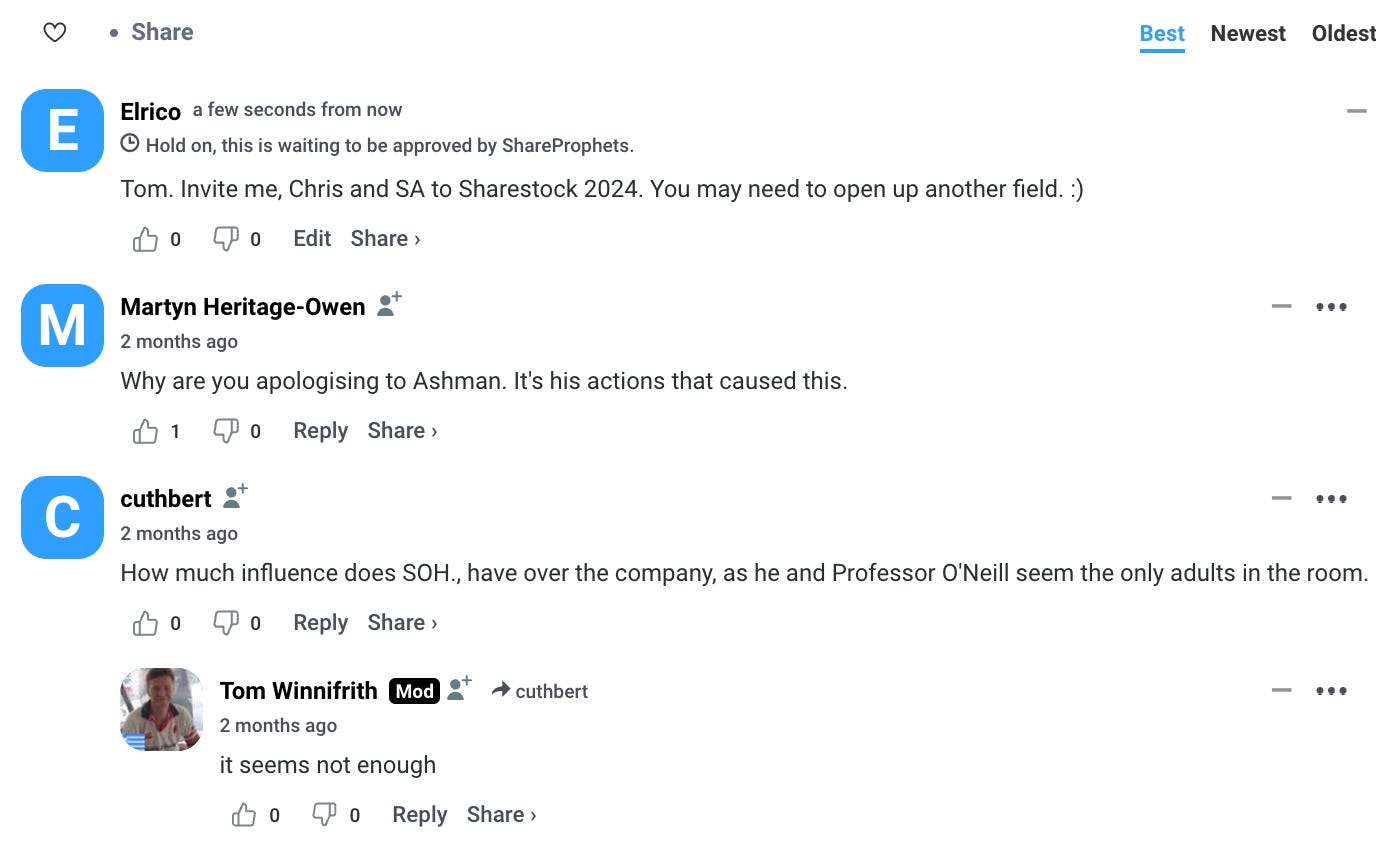

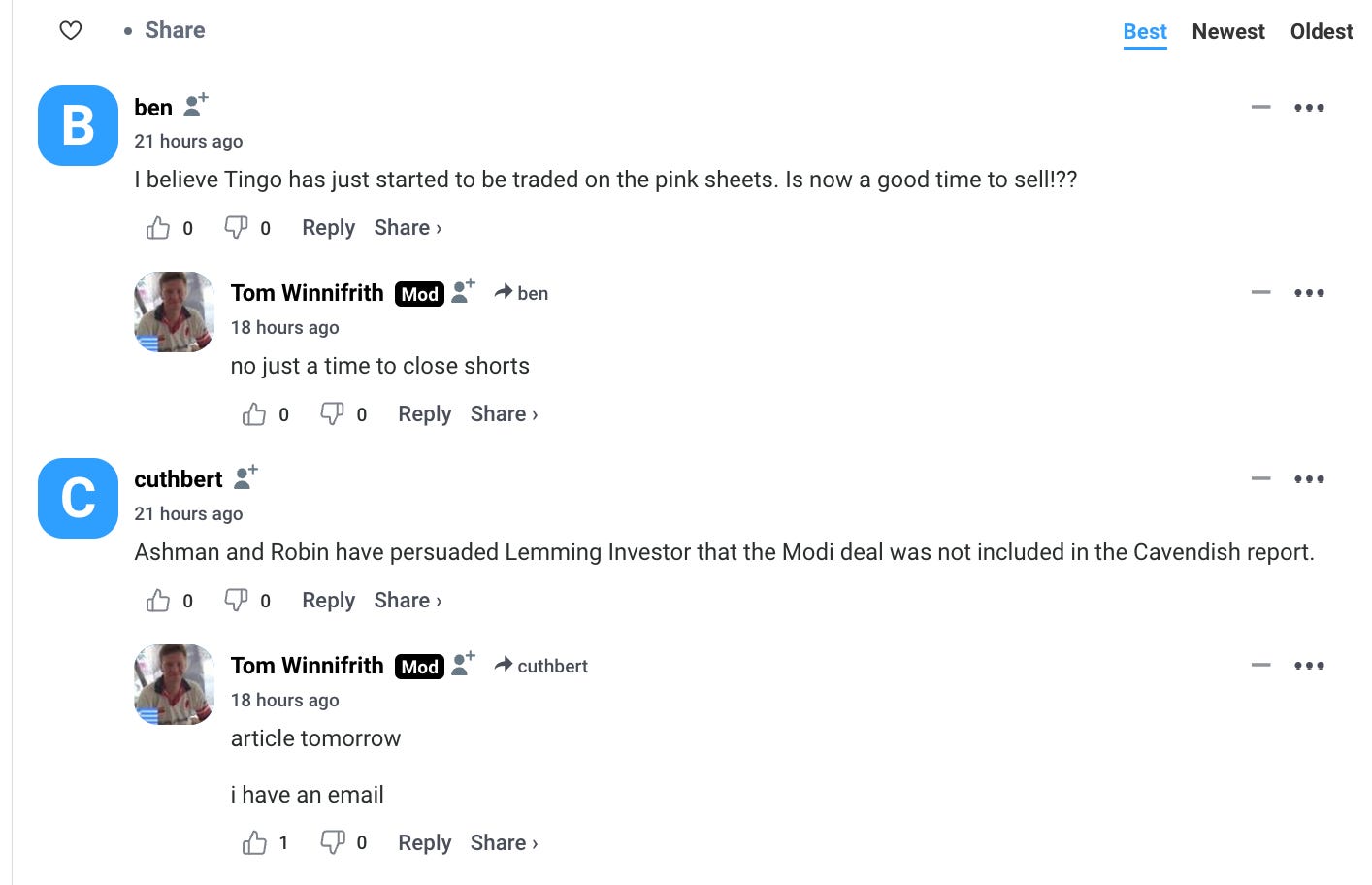

More revelations are on the horizon in this unfolding drama. To those who have been following closely, my assertion that the recent announcement about Dermatonics and its partnership with the Umesh Modi Group to launch Pheet and Dermatonics Once Heel Balm across Asia, the Middle East, and Africa was conspicuously absent from Cavendish's broker forecasts has been a point of contention. Critics, including the vociferous Mr Angry, have quickly dismissed my hypothesis, with some even suggesting that my grasp on the nuances of RNS reports and broker analyses pales compared to their seasoned expertise.

Yet, I stand firm in my conviction, undeterred by the naysayers. The depth of my analysis and the rigour of my inquiries, particularly those directed to CFO Manprit Singh Randhawa and his answer, vindicates my hypothesis. The unfolding events may well vindicate my stance, underscoring the value of a thorough and independent examination of the facts over the cacophony of conventional wisdom.

Tom's point is well-taken; given the deal inked in June 2023, the Cavendish analyst would have indeed incorporated his valuation, though likely excluding 2024, as the product's early launch was unforeseen. My discussions with Tom have centred on why the analyst might have omitted his deal valuation for 2024. However, the real crux of the matter lies in debating whether the analyst's projections have erred on the side of excessive caution.

Obviously, clarity was needed, and clarity has been provided by the CFO.

Question to Ashman and Randhawa

Gentlemen, I've previously shared my observation that the announcement of Dermatonics partnering with the Umesh Modi Group for the launch of Pheet and Dermatonics Once Heel Balm in Asia, the Middle East, and Africa is not contained in Cavendish's broker forecasts.

Could you kindly verify if my observation is accurate? Should this be the case, it would directly challenge the narrative of a three-year financial drain on the Company, as proposed by Tom Winnifrith. This would not only lend credibility to the strategic merit of the Dermatonics acquisition but also suggest a rather timely advantage, given the implication of an "imminent launch" rather than a protracted timeline of months or even years.

Answer: Randhawa: Vindication, or ouzo-time, as Mr Angry would shout!

“Further to the recent announcement of RNS about the licence agreement with the Umesh Modi Group and the potential of this deal in the current and future years, I can confirm that the analyst forecasts that are currently in the market do not contain any revenue forecasts associated with this licencing agreement.”

“The original expected launch date was unknown to the Dermatonics team as we conducted diligence on the business last year. As a result, we felt it inappropriate to issue forecasts post-completion due to the uncertainty of the timing of the launch.”

“The rapid launch date, which caught both the Dermatonics team and us off guard, forced us to make the announcement, and as the Modi team prepares for launch, we are working with them to understand forecasts over the coming months and years. We will then issue these to the market.”

I should add, UMG has launched the heel balm today!

Seeing my hypothesis confirmed is immensely satisfying, far beyond mere relief. This holds especially true after the intense debates I've had with several individuals, Tom included. SkinBioTherapeutics hasn't released a corrective RNS because they are not in a position to provide a forecast until an audit. Considering the undue criticism around the Dermatoncis acquisition Ashman and Randhawa have faced, it's the logical move. I'm particularly keen to observe Tom's reaction upon realising that his 34 years of analytical experience have surprisingly missed the mark here. It's as if a lemming has outwitted Mensa, piecing together the puzzle just as I take the plunge!

Randhawa continues

In our 20 February RNS announcement about the licence agreement with the Umesh Modi Group and the potential of this deal in the current and future years, we made it clear that “This collaboration is currently at an early stage, therefore, management does not expect any changes to current market expectations at this stage.” If that is not clear, I can confirm that this means that a) the analyst forecasts for the enlarged group are not currently in the market and that those that go out to June 2024 do not contain any revenue forecasts associated with this licencing agreement and b) the analysts’ stand alone Dermatonics forecasts (which go out to June 2026) in the research note of 2 February do not contain any revenue from this agreement.

The original expected launch date was unknown to the Dermatonics team as we carried out diligence on the business last year, and the levels of revenue uncertain, as a result, the analysts forecasts post-completion are on growth within the Dermatonics business .

As the Modi team have now launched, we are working with them to understand forecasts over the coming months and years, and will look to update guidance to the market.

With regards to the acquisition of Dermatonics, it is an earnings accretive transaction. In the analyst note of 2 February forecast EBITDA for the years 2024, 2025 and 2026 (year ended June to align with the Group’s year end of 30 June 2024) is £450k, £560k and £650k respectively, reflecting growth in the NHS revenues as well as international distributor. As noted above, it is expected that any earnings from the Modi deal would be in addition to this and we will look to update guidance to the market once we have clarity on the forecasts.

From a cash flow perspective £450k generated in 2024 and £500k of the £560k EBITDA generated in 2025 and £250k of the £650k EBTIDA generated in 2026 will be used to fund deferred consideration payments to the sellers. The excess EBITDA of £400k generated in the year to 31st January 2026 and the EBITDA generated from February 2026 onwards will be free cash flow into the business thereafter. And again, any cash flow generation from Modi will be cash flow and earnings enhancing in the financial year 2024/2025 and beyond.

Continuing with Tom’s bearcast: Indeed, the echoes of Tom’s concerns mirror my conversations with Stephen O’Hara of OptiBiotix Health. Despite O’Hara’s regard for Ashman, the tides of dissatisfaction with the company’s strategic direction and funding avenues are rising. As an investor in SkinBioTherapeutics, the prospect of being ousted by Ashman and the Randhawa sends a shiver down my spine. The murky depths of financial machinations, so often shadowed by back-stabbing and conspiracies, are at play here, threatening to swallow two pivotal figures in a whirlpool of corporate intrigue.

The concerted efforts to dislodge board members leave me both saddened and perplexed. The recent fiasco surrounding convertible bonds (CBs) has only fueled the fire, sparking a storm of discontent among shareholders. My endeavours to voice my concerns to Ashman and Randhawa have been relentless, yet the barrage of criticism they face, from public outcries to more covert manoeuvres, is disheartening.

My stance remains unwavering amidst the cacophony of voices eager to school me on the dangerous “death spiral” of CBs. Unlike Tom, with his activist journalistic fervour, my domain lies within education and research, peppered with personal insights. While I may not wear the activist badge openly, my behind-the-scenes efforts to advocate for change are no less sincere.

Tom spins a narrative suggesting OptiBiotix might swoop in to acquire SkinBioTherapeutics for a pittance, which is not just disheartening but feels like a calculated move to undermine confidence. This tactic, aimed at pressuring the board, seems designed to precipitate a moment of reckoning while accelerating the erosion of shareholder value. In these trying times, the feeling of helplessness in the face of such orchestrated campaigns is palpable, leaving one to ponder the future with a heavy heart.

Amid this turmoil, I must acknowledge that mistakes, significant ones at that, have been made by the team at SkinBioTherapeutics. Yet, amidst the whirlwind of criticism, I discern a genuine effort on their part to rectify these missteps, albeit in ways that might not entirely align with our expectations. The muddied waters of contradictory official statements do little to dispel the fog of uncertainty, casting an unwelcome shadow over the company’s trajectory.

Furthermore, while Tom asserts his seasoned perspective outweighs both mine and Ashman’s, dismissing my understanding of the intricacies behind broker notes and their analytical foresight, I’ve managed to delve into specifics that shed light on certain oversights. Notably, the absence of Dermatonics and the Umesh Modi Group (UMG) from the Cavendish note stands out, a point I’ve pinpointed not due to an anticipated immediate product launch as the recent RNS might suggest, but rather through a careful analysis of the language used: “In the meantime, we are swamped integrating the recently acquired Dermatonics, the accelerated Modi/Dermatonics product launch in the Asia, Middle East and Africa regions.” This hints at an unexpected acceleration, perhaps not even fully anticipated by the board.

Investors, seasoned in the timelines of OptiBiotix’s partnership ventures, understand all too well the protracted journey from agreement to actual product launch—often spanning months, if not years. This backdrop fuels my belief that the rapid progression towards the UMG product launch may have surprised the board. Now, more than ever, a swift and clarifying update is imperative to validate this theory. The longer the narrative of Dermatonics being a financial sinkhole, as Tom suggests, persists without rebuttal, the heavier the burden on the board to counteract this mounting pressure with transparency and decisive action.

A glimmer of hope remains anchored in the tangible successes of Dermatonics. Last year, Dermatonics brought in revenues of £1.82 million, a testament to its potential and prowess in the market. Yet, the prospect of breaking new ground with another foray into the USA market, coupled with the promise of enhanced synergies and margins, seems to be conveniently overlooked by those naysayers with ulterior motives. This oversight not only undermines the achievements and potential of Dermatonics but also fails to recognise the strategic value it adds to SkinBioTherapeutics. The cynics may ignore this facet, but the numbers speak volumes about the untapped opportunities and the resilience of this newly forged alliance in the face of adversity. It seems the angst around the CBs trumps the Dermatonics and UMG partnership that promises further collaborations.

There's unmistakably a game of power at play here, though the ultimate goal and the maestro behind it remain elusive. But make no mistake, it's not just us investors bearing the brunt of the fallout. On forums, some sly individuals are trying to dupe less experienced investors with tactics that could exacerbate losses, anticipating a further 25% plunge in the share price. This overlooks the transient nature of this emotionally charged period, which, once dissipated, will reveal the true value of the Dermatonics acquisition and the promising developments on the horizon, heralding a return to stability.

Heaven forbid if our dear friend Putin decides to send a nuclear postcard in our direction, a token of his heartfelt gratitude towards the dazzling brilliance of our political maestros. These paragons of virtue, who seem to have misplaced their diplomas from the School of Diplomacy and Commonsense, might just have outdone themselves and provided us with something far more serious to worry about other than CBs.

Secrete Leftie Censorship - Exhibit One :)

There was a third, which does not show on the “pending” list. So, either moderation is slow to catch on, or one has been refused another.

Opinions

We offer no advice or solicit the purchase of shares in any companies we discuss. However, shares go up and down in value, making your financial situation risky.

The views and opinions contained within these editorials are for research purposes and are the opinions of the author(s). We aim to be as accurate as possible but stress you should also perform your research and never act solely on the contents of these editorials.

elrico, tw has put your posts up on share prophets. Interestingly the time stamp makes it look like you were wrong, as i also. Its a good job you grabbed them because it does look like tw tried to reel you in to make a fool of you as vengence for making him look a fool of 34 year.

Elrico, i have just checked the comments section on share prophets. Your censorship is proof tw is feeling uncomfortable with your update because it proves he is wrong. It is interesting to read his rant today. It mentions an email from someone. It mirrors yours so it suggests multiple people have asked the same question and got the same answer. Tw focuses on his victimhood again while ignoring the elephant in the room. He deflects from the fact he is wrong and you have been proven right.

Well done. I wish you had conformation earlier because i sold some sbtx to but opti. I'm not blaming you.