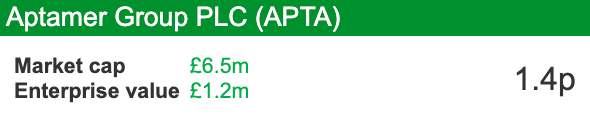

Aptamer Group plc

prodigal Son Returns, New Funding, Cost Cutting - Recovery Hope or Lost Cause?

By Elric Langton | 28 October 2023

Today's featured company embodies the profile of a classic early-stage disruptor, a resilient small-cap contender in the life sciences arena with potential risks and rewards we strive to discover, research and report on for you.

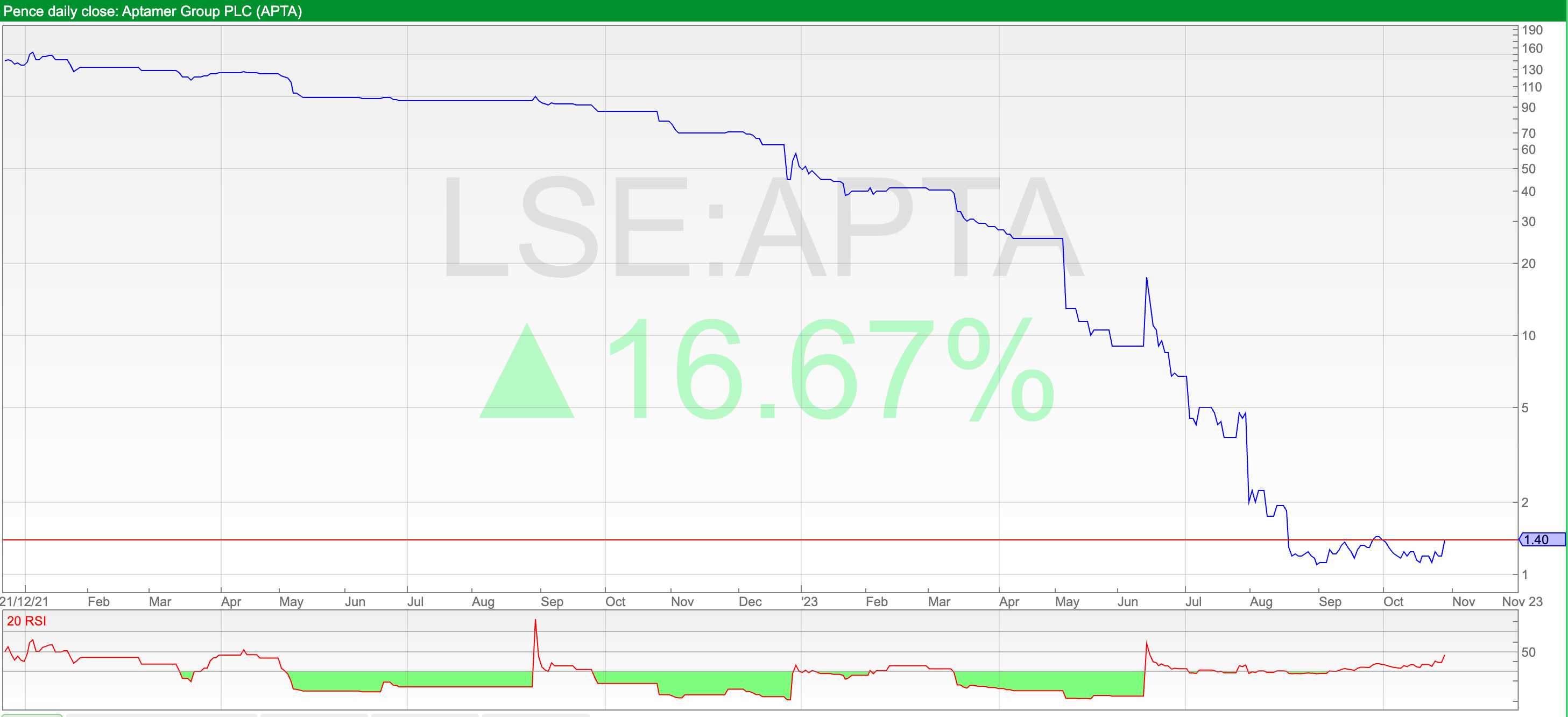

Aptamer Group has fallen from on high, not even a rollercoaster, just the lemming-like plunge off the cliff 150 meters high, figuratively speaking (150p to 1.1p in less than two years), to ground zero-well, almost. Even so, the fall from IPO listing in December 2021, raising £10.8 million at 117p valuing the Company at £80 million, Hence, it is not without its considerable risks associated with a Company in the life sciences, throw in a profit warning and board restructuring and include a prodigal son return, I almost threw it off my watchlist.

In the unpredictable London’s junior casino, where the rollercoaster rides can be sickening with capricious volatility, there emerge stories of resilience and reinvention. Aptamer Group a MedTech firm headquartered in York, is one such narrative, poised on the precipice of a remarkable resurgence, or so is the belief of its army of battered investors. With a visionary boardroom reshuffle, the appearance of a robust financial restructuring plan, and successful fundraising, Aptamer Group is positioning itself as a compelling bet in the dynamic life sciences sector that will force me to commit to an initial position, likely to be as early as next week.

Aptamer is a pioneering MedTech firm specialising in synthetic antibodies developed through their exclusive Optimer technology. Their primary focus is on providing Optimer® binders for research, diagnostics, and therapeutics, offering tailored and innovative solutions for professionals in the life sciences industry.